Investment objective

The investment objective is to generate superior returns for Unit holders by investing in global markets, with a focus on reducing risk and preserving capital.

More information can be found in the Information Memorandum located at the Fund website.

Applications available here.

Investment Strategy

The Defender Global Fund (Fund) provides investors with exposure to global markets through a long and short strategy.

The Fund starts with the Managers global macroeconomic and market outlook , then overlays key thematics which the Manager believes will effect future performance and combines this with a bottom-up investment decision criteria.

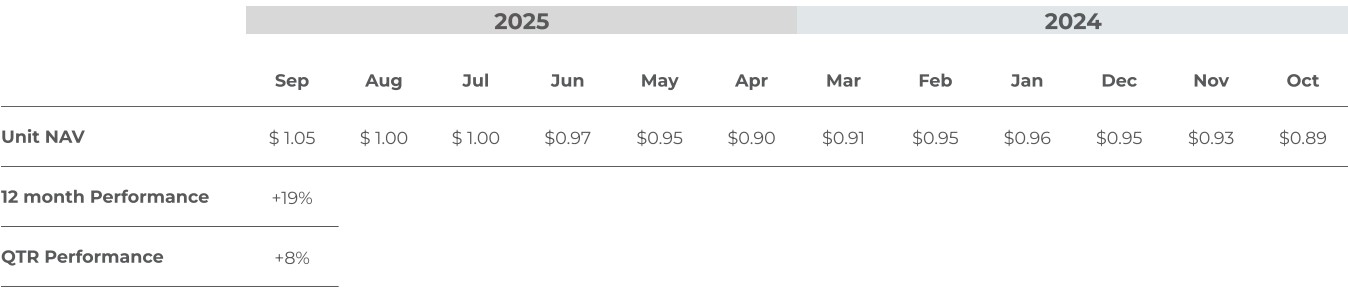

Performance Summary

Commentary

The Defender Global Fund returned +8% in Q3 CY2025.

Financial Markets Report: Q3 CY2025

The third quarter of 2025 (Q3 2025) marked a pivotal shift in the global financial landscape. While 2024 was defined by “AI Hype,” Q3 2025 will be remembered as the beginning of the “AI Monetization” era. The US markets reached new record highs, driven by a resilient economy and a re-acceleration in enterprise technology spending, while the Australian economy showed surprising resilience despite persistent global headwinds.

US Market Overview: A Bull Run Built on Fundamentals

The US equity markets maintained a bullish trajectory throughout the quarter, with the S&P 500 rising 8.1% and the tech-laden Nasdaq Composite rallying 11.2%. This performance was supported by the fourth consecutive quarter of double-digit earnings growth for S&P 500 companies, which grew at a collective rate of 14% well ahead of initial analyst expectations.

Small-cap stocks also saw a long-awaited “rotation” rally, with the Russell 2000 surging 12.4% as the Federal Reserve initiated its rate-cutting cycle in September. This shift signalled investor confidence that the US economy was heading for a “soft landing” rather than a recession.

The “Big Five” Tech Analysis: Engineering the AI Era

NVDA (NVIDIA): The AI Factory Revolution NVIDIA continued to dominate the global conversation, reporting a staggering $57 billion in quarterly revenue a 62% increase year-over-year. Under the leadership of Jensen Huang, the company transitioned its narrative from selling chips to building “AI Factories.” Data center revenue accounted for $51 billion of the total, as hyperscalers aggressively deployed the NVIDIA Blackwell (B200/B300) architecture. Despite supply chain complexities, NVIDIAˇs gross margins remained robust at 73.4%, reinforcing its position as the primary architect of the accelerated computing era.

GOOG (Alphabet): The First $100 Billion Quarter Alphabet reached a historic milestone in Q3 2025, delivering its first-ever $102.3 billion revenue quarter. Google Cloud was the standout performer, with revenue accelerating 34% to $15.2 billion, driven by deep integration of Gemini 2.5 Pro across its enterprise suite. The Gemini App now boasts over 650 million monthly active users, and Alphabetˇs “full-stack” approach to AI from custom TPU silicon to consumer-facing applications appears to be yielding significant operational leverage.

MSFT (Microsoft): Cloud Prowess and Capacity Limits Microsoft reported $70.1 billion in revenue, representing 13% growth. Its “Intelligent Cloud” segment grew 21%, led by Azure and other cloud services at 33% (35% in constant currency). Satya Nadella highlighted that AI now contributes 16 percentage points to Azure’s growth. However, the quarter also revealed a “high-class problem”: Microsoft remains supply-constrained in specific geographies, with demand for AI compute capacity exceeding the company’s current ability to provision hardware.

AMZN (Amazon): AWS Re-acceleration and the Capex Challenge Amazon saw a powerful re-acceleration in AWS, which grew 20.2% to reach a $132 billion annualized run rate. CEO Andy Jassy noted that AWS momentum is at its highest level since 2022. However, the market focused heavily on Amazon’s capital expenditure, which hit $34.2 billion for the quarter. With a full-year 2025 capex estimate of $125 billion, investors are closely monitoring the balance between massive infrastructure outlays and the timing of free cash flow returns.

META (Meta): The Cost of Superintelligence Meta delivered a mixed but resilient quarter, with revenue growing 26% to $51.2 billion. The companyˇs core advertising business remains exceptionally healthy, with ad impressions rising 14%. However, Meta reported a significantly lower EPS of $1.05 (vs. expected $6.70) due to a one-time non-cash income tax charge of $15.9 billion. Mark Zuckerberg continues to signal an aggressive path forward, raising 2025 capex guidance to $70 72 billion to support “Meta Superintelligence Labs” and next-generation wearables.

Macroeconomic Commentary

The US Economy: The “Jobless Expansion” The US economy defied gravity in Q3, with Real GDP increasing at an annual rate of 4.4% the strongest advance in two years. This growth was fueled by robust consumer spending and a surge in AI-related business investment. However, a unique “jobless expansion” emerged: while GDP grew, monthly job growth remained sluggish at approximately 30,000, as firms utilized AI to drive productivity gains rather than hiring. PCE inflation hovered near 2.8%, allowing the Fed to begin its pivot toward a more accommodative policy stance.

The Australian Economy: Resilience Amidst the Speed Limit The Australian economy gathered momentum in Q3, with GDP growing 0.4% for the quarter and 2.1% annually its strongest performance in two years. The main drivers were government infrastructure spending and a rebound in household consumption, spurred by the Stage 3 tax cuts which finally reached consumersˇ pockets. While the construction sector remained a drag due to cost pressures, business investment in digital infrastructure and data centers provided a significant productivity boost. The RBA maintained a cautious stance, with a cash rate of 3.35% expected by year-end as headline inflation moderated to 2.4%.

Outlook for Q4 and Beyond

As we enter the final months of 2025, the central theme remains the durability of the AI investment cycle. While “capex anxiety” persists, the underlying fundamentals of the “Big Five” suggest that the transition to accelerated computing is still in its early innings. Investors should watch for the impact of global trade policies and the continued divergence in labour markets as AI-driven efficiency becomes a core macroeconomic driver.€ And as an aside, this report was written with the assistance of Googleˇs Gemini LLM. GOOG remains a core holding in the DGF portfolio.

Regards,

The Defender Global Team

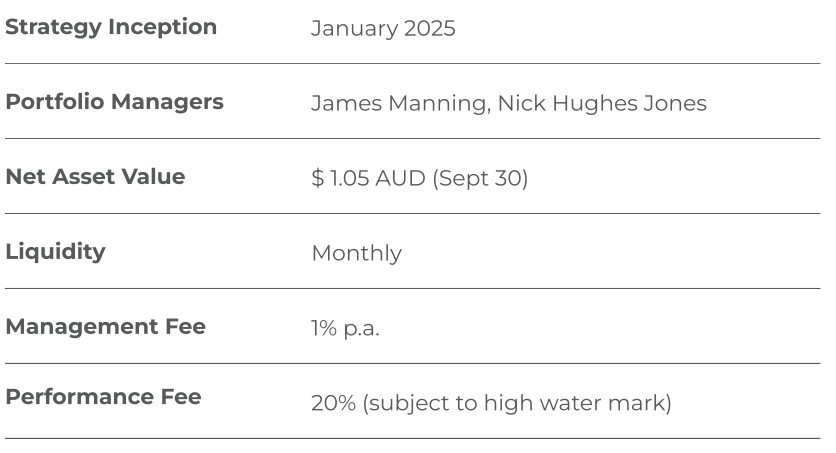

Key information

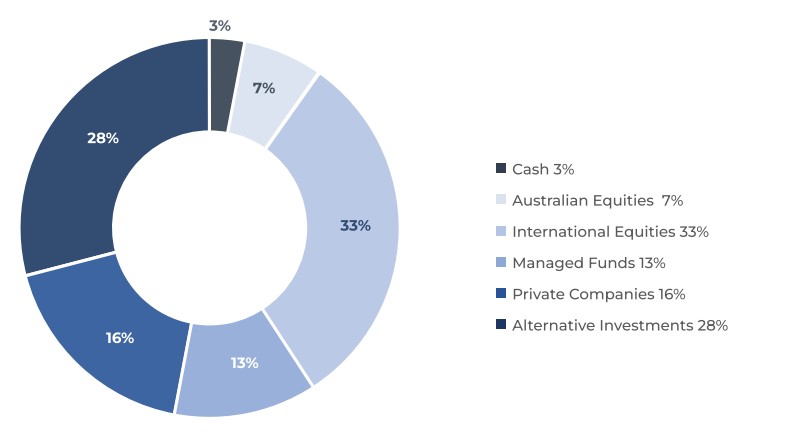

Sector allocation

2 October 2025

Important Notice

This report has been prepared by Defender Capital Pty Ltd ABN 58 636 314 540, operating under a Corporate Authorised Representative agreement of Defender Asset Management Limited (AFSL 482722) (CAR 001 285 563), Fund Manager of the Defender Global Fund (ABN 27 482 997 023) without taking into account the objectives, financial situation or needs of individuals and is prepared only for wholesale investors. Before making an investment decision about the Fund, investors should read the Fund’s Information Memorandum available at the Funds website https:// defenderam.com/investments/ or by contacting [email protected] and obtain advice from an appropriate financial adviser. Units in the Fund are issued by Defender Asset Management Limited (ABN 29 608 281 189) (AFSL 482722).

his information is current as at the date of publication. The material has been prepared based on information believed to be accurate at the time of publication. Assumptions and estimates may have been made which may prove not to be accurate. Defender Capital undertakes no responsibility to correct any such inaccuracy. Subsequent changes in circumstances may occur at any time and may impact the accuracy of the information. To the full extent permitted by law, neither the Fund Manager, the trustee or any related entities makes any warranty as to the accuracy or completeness of the information in this newsletter and disclaims all liability that may arise due to any information contained in this newsletter being inaccurate, unreliable, or incomplete. Past performance is not a reliable indicator of future performance.